Cheap Money with an Eastern Accent

26.06.2026 10:00

Cheap Money with an Eastern Accent

How China’s years-long battle with deflation delivered record-cheap financing for Kazakhstan - and what it reveals about the new geometry of global power

At the end of May 2026, something happened in Beijing that only five years earlier would have looked like a typo in a financial market bulletin. The Republic of Kazakhstan - Central Asia’s largest economy - placed three-year bonds in China’s market for 3.4 billion yuan, around $500 million, at 1.9% per annum. Rates of that kind are normally reserved for countries with AA-level credit ratings. The order book was twice covered.

To understand how Astana managed to borrow more cheaply than its credit rating would imply, one should look not only at Kazakhstan. One should look at China - and at what has happened to the Chinese economy over the past five years.

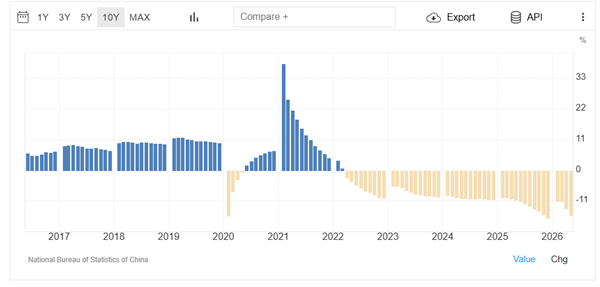

The Year Something Broke

The turning point came in 2021. Until then, China’s real-estate market, technology sector, consumer sector and export industries had all been growing powerfully. In 2021, technology, consumption and property were hit at the same time.

First to come under pressure were the technology champions. Regulatory pressure, which had begun with the sudden halt of Ant Group’s record IPO and the antitrust investigation into Alibaba, quickly spread across the sector - from online education to video games. Investors who only recently had seen the Chinese internet as the showcase of the new economy began to head for the exits, and valuations of the technology giants crumbled.

Almost immediately, a second and much deeper crack appeared: real estate. For decades, housing had been the principal store of savings for Chinese households and, for developers, a machine for producing debt. When the authorities tightened borrowing rules, the largest developers, led by Evergrande, found themselves on the brink of default. A bubble inflated over years began to deflate - slowly, painfully and in public.

The effect was less financial than psychological. The Chinese consumer, whose wealth was tied to the value of an apartment, felt poorer for the first time in a generation. Confidence fell, savings rose, spending contracted. Car sales headed lower, while the effect of one-off subsidies for durable goods quickly faded. An economy accustomed to high growth entered an unfamiliar state: deflation appeared on the horizon - not rising prices, but falling ones. For most countries that sounds exotic; for an economy loaded with debt, it is a dangerous diagnosis, because when prices fall, the real burden of debt rises.

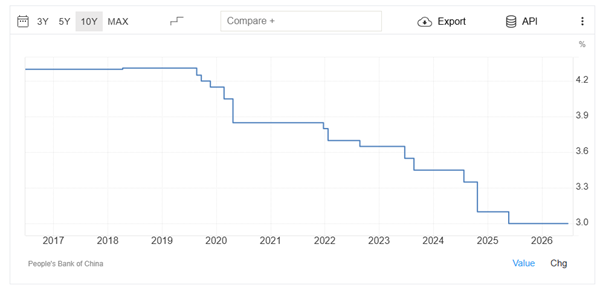

Beijing Opens the Taps

The authorities’ response was predictable in direction but impressive in scale. Over the past two years, the People’s Bank of China under Pan Gongsheng has steadily eased policy, flooding the economy with cheap liquidity.

The logic is simple: if confidence does not return on its own, money must be made as cheap as possible. Over the years of the current five-year plan, China’s central bank has cut banks’ reserve requirement ratio nine times, releasing around 7 trillion yuan of long-term liquidity into the system. The culmination was a ten-point package announced in May 2025: a cut in the key rate on seven-day operations, another reduction in reserve requirements worth nearly a trillion yuan, targeted lending programmes for consumption and the technology sector running into the hundreds of billions, and cheaper mortgages. By early 2026, the regulator was making clear that there was still room for further action.

The result of this prolonged accommodation is an ocean of yuan looking for a home, and interest rates inside China pinned close to historic lows. Money in China has never been cheaper. The only question was where it would flow.

Three Doors Out of Deflation

China has, in effect, three ways out of the trap of cheap prices and high debt: spur innovation to raise productivity, restructure accumulated debt, and expand into external markets. It is the third door that has proved the widest - and the most important for its neighbours.

Property investments in China

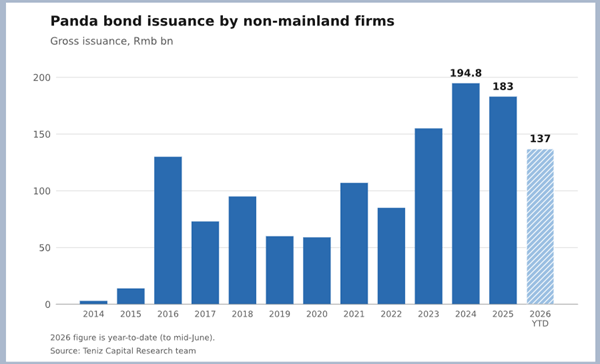

When domestic demand stalls, Chinese companies go abroad more actively: building factories, supplying equipment, taking equity stakes in projects, financing trade flows - and, increasingly, doing all this in yuan. At the same time, Beijing has methodically been building the financial infrastructure for its own currency. CIPS, the Cross-Border Interbank Payment System - China’s answer to Western clearing systems - by 2025 linked almost 200 direct participants and more than 1,500 intermediary banks, covering more than 120 countries; annual transaction volume exceeded 180 trillion yuan. To this were added two bond markets: panda bonds, which foreign issuers sell onshore in China, and dim sum bonds, placed offshore in Hong Kong. Both allow foreign governments and companies to borrow directly in yuan.

In other words, China exports more than goods. It exports capital, engineering expertise and its own currency. And it needs countries willing to accept all three.

Kazakhstan Fits the Bill

Kazakhstan fits this logic almost perfectly. A shared border, a rich raw-material base, transport corridors between China and Europe, metallurgy, energy, agriprocessing - for Chinese capital, it is a convenient and comprehensible platform. It is no accident that China has already become the country’s largest trading partner: bilateral trade has exceeded $30 billion, while China’s share of Kazakhstan’s foreign trade is approaching one-third.

This turn is easy to see on the ground. In Zhambyl Region, Fufeng Group is building a deep corn-processing plant with investments of around $1.5 billion. In Atyrau Region, Sinopec is participating in a polyethylene project worth roughly $7.4 billion. And in Abai Region, an agreement has been signed to build a $1.5 billion copper smelter, where Chinese companies are responsible for engineering, equipment and construction - and where financing is planned precisely through a yuan-denominated bond issue. Chinese capital is moving ever more visibly from the simple export of goods to high-value-added industrial projects on Kazakh soil.

It is important to understand that in this relationship Kazakhstan is not a supplicant, but a partner with something to offer. It is the largest economy in Central Asia and the country with the highest GDP per capita among all its neighbours, including the former Soviet republics. Its mineral wealth has long been open to the world’s strongest players: the largest oilfields - Tengiz, Kashagan and Karachaganak - have for decades been developed together with American and European majors, and that Western capital remains in the country. At the same time, Kazakhstan is not under sanctions, retains direct access to advanced technologies - from Nvidia chips to industrial equipment - and is actively building data centres, turning itself into a regional technology and energy hub. This is why the country can do business on equal terms with Washington, Moscow and Beijing at once: multi-vector policy here is not a slogan, but real negotiating power.

China’s Loan Prime Rate

But the truly new element has been the financial channel. In less than a year, Kazakhstan has covered ground that takes other countries years.

A Yuan Ladder

The first to enter the yuan market, in September 2025, was the Development Bank of Kazakhstan, which placed 2 billion yuan of securities at 3.35%. A month later, KazMunayGas made its debut: the national oil and gas company borrowed 1.25 billion yuan for five years at a 2.95% coupon, securing its lowest yield on record and access to a new pool of Asian investors. In the spring of 2026, Samruk-Kazyna placed the first panda bonds in the history of Kazakhstan and all of Central Asia - 3 billion yuan at 2.18%. And in May, the Ministry of Finance capped the sequence with its sovereign issue at the same 1.9%.

Notice one detail: rates fell with every issue. As the market gradually became familiar with Kazakh risk, it priced that risk more cheaply. Each subsequent placement rested on the confidence earned by the previous one - and there is a certain elegance in that sequence. First a development institution, then a national company, then a sovereign wealth fund and finally the state itself: four layers of Kazakh risk formed a neat ladder that other issuers can now climb.

Why Kazakh Borrowers Need the Yuan

As Teniz Capital’s analysts have noted in their research, the significance of these deals goes beyond their nominal size. Taken together, the four issues amount to less than 10 billion yuan - modest beside the country’s dollar, euro and tenge debt. But they have for the first time built an entire “ladder” of Kazakh risk in the yuan market, creating a foundation for future placements.

The economic rationale for yuan debt is especially clear wherever a project has a “Chinese component”. If a plant is built with Chinese equipment, by Chinese contractors, and its output is later exported to China, it makes more sense to service the debt in yuan: costs and liabilities are in the same currency, reducing foreign-exchange risk.

Teniz Capital, whose analysts were among the first to describe this structural shift as an investment theme in its own right, is not merely an outside observer: the firm works with the same yuan instruments as the country’s largest issuers, testing its conclusions through its own participation in the market. This is one of those cases in which research insight and practical experience reinforce one another.

A New Geometry of Power

Behind the financial mechanics lies a much larger story - about how the map of influence is changing.

While the United States is waging military campaigns in the Middle East and arguing over tariffs with its closest neighbours, Canada and Mexico, China is doing something fundamentally different. It is building trust. Not with tanks or sanctions, but with factories, credit lines, joint projects and cheap money. This is “soft power” in its most practical form: a neighbouring country gains access to affordable financing, jobs and infrastructure - and becomes more deeply embedded in the orbit of the Chinese economy. Capital turns out to be more persuasive than rhetoric.

This strategy has an important feature: it is designed for decades, not electoral cycles. China rarely demands that its partners make an immediate political choice and almost never attaches ideological conditions to its money. It offers developing economies what they need here and now - capital, technology, access to export markets - and patiently waits for mutual benefit to bind the parties more tightly than any declaration. For its neighbours, this makes Beijing a predictable and, in a sense, convenient counterparty: one with which they can plan for the long term, because they understand the logic of its interests. It is this predictability, rather than the size of its wallet alone, that is the chief resource of China’s soft power - patient, pragmatic and therefore particularly persuasive.

The same shift is visible beyond raw materials and infrastructure. In April 2026, Chinese technology giant Tencent - the company that, in effect, created the very model of the super-app - acquired around 3.2% of Kazakhstan’s Kaspi.kz for roughly half a billion dollars, entering the country’s fintech sector for the first time. For Tencent, this is only its second move into Central Asia after Uzbekistan’s Uzum, and the logic is the same as in large industrial deals: find a profitable regional leader in a growing market and become part of it for years to come. Significantly, Chinese capital entered Kaspi not alone, but alongside American institutional investors and university endowments, while the company itself remained listed on Nasdaq. Beijing’s growing presence in emerging markets - and in Kazakhstan in particular - is not so much displacing Western players as taking its place alongside them. For countries like Kazakhstan, that coexistence is precisely where the benefit lies.

Panda bond issuance by non-mainland firms

For Kazakhstan, there is neither naivety nor one-sided dependence in this. The yuan is not replacing the dollar, the euro or the tenge; it is adding another channel, another pillar to the country’s traditionally multi-vector policy. But the direction of travel is clear. In a world where one superpower increasingly projects strength through conflict, another projects it through capital. And small economies - from Central Asia to Southeast Asia - are increasingly voting for the one that arrives with a construction site, not an ultimatum.

Back to Beijing

Let us return to that figure: 1.9% per annum. In itself, it is dry and technical. But behind it lies the logic of an era. China, fighting its own deflation, made money cheap and sent it abroad. Kazakhstan, having spent years building a reputation as a disciplined borrower, was ready to accept that money - and did so on terms that far richer countries would envy.

If this trend continues - and for now everything suggests that it will - the yuan may become a working currency for Kazakhstan’s trade settlements, project finance and long-term borrowing. Not instead of the familiar currencies, but alongside them. A story that began with a burst bubble at the other end of the continent has unexpectedly become a new financial opportunity for Astana. And judging by the speed with which Kazakhstan has seized it, no one here intends to let that opportunity pass.